Introduction to Chargebacks

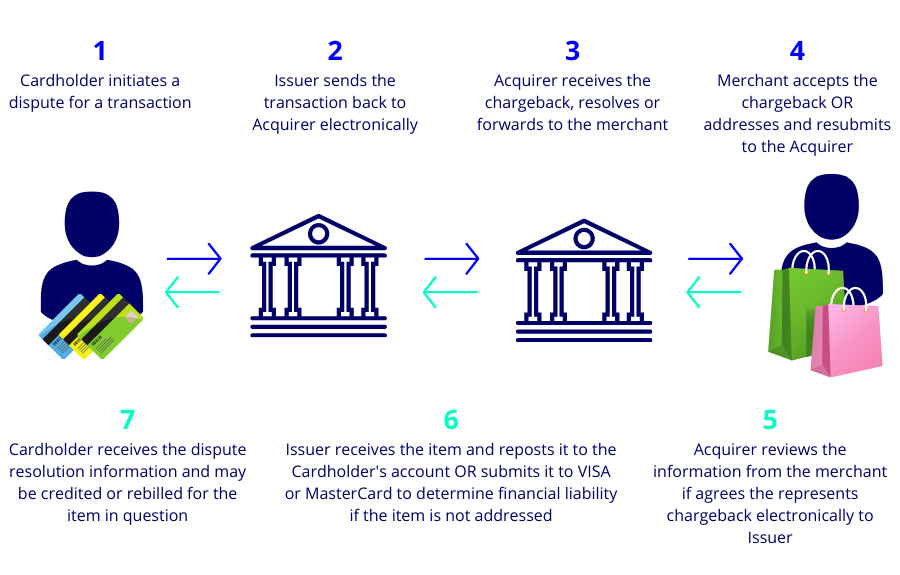

A credit or debit card chargeback is the return of money from a card transaction back to the cardholder. The chargeback simply reverses the payment or money transfer from the consumer’s credit or debit card. A chargeback can be initiated by the Card Issuer i.e. the Bank that issued the debit or credit card either at the request of the cardholder or when the Issuing bank sees the need to do so via the Card schemes e.g. Visa or Mastercard.

Common reasons for chargebacks / reversals are:

- Cardholder denies authorising a transaction e.g. a fraudulent transaction

- Cardholder does not recognise a transaction

- Cardholder disputes the sale for reasons such as failure to receive goods or service

- Cardholder disputes the sale for reasons of quality

All Merchants accepting debit and credit card payments run the risk of being liable for chargebacks. A cardholder or card Issuer has the right to question or dispute a card transaction. A chargeback can be received up to 120 days after the card transaction was taken. In the case of goods or services being delivered, a chargeback can be raised up to 120 days from agreed date of delivery.

Common Misunderstandings

A card authorisation is a guarantee of payment

An authorisation proves the card has sufficient funds available at the time of transaction and / or the card has not been reported stolen at the time of the transaction. It does not vouch for the validity of the person using the card and is not a guarantee of payment.

All chargebacks can be defended

Unfortunately they cannot. The reason cited by the cardholder for the chargeback will mean that the cardholder’s bank can immediately issue a Chargeback. Some Chargebacks cannot be defended and in these cases your nominated account will be debited by BOIPA for the value of the Transaction. Visa and MasterCard define a number of ‘reason code’ categories for disputes raised by cardholders. It is the reason code that determines if you have an opportunity to defend the dispute, or if it will be an automatic Chargeback. This means you will sometimes be contacted with a request to provide evidence, and sometimes your account will simply be debited for the Chargeback.

What happens if a chargeback can be defended

If the Chargeback can be defended, BOIPA will contact you via email containing instructions for providing the evidence needed to prove the Transaction was legitimate. The email will also contain a deadline for responding. If the evidence you submit is insufficient, or submitted after the deadline, the dispute will result in the value of the Transaction being charged back to you. The key for you is to always follow the instructions in any correspondence you receive from BOIPA regarding retrievals or Chargebacks and always submit your responses by the required deadlines.

Why are there charges for processing chargebacks?

Processing chargebacks incurs a fee due to the administrative work required on the part of BOIPA in requesting and providing supporting documentation to the schemes.

Summary

BOIPA always works with its merchants to decrease their fraud and chargeback levels. Merchants are also required to monitor their fraud and chargeback levels, and adapt business practices accordingly, to ensure fraud and chargeback levels are at an acceptable level. If a merchant would like further clarification on any issue related to fraud or chargebacks, they can contact BOIPA and we will work with you to find an optimal solution.

For more information on Chargebacks please refer to your Payment Acceptance Agreement or contact our Customer Care team on 1800 806 670 or [email protected].